- Finovatic - The Capsule of Finance

- Posts

- Macro-Economic Analysis focusing on pre-release data & smart money movements

Macro-Economic Analysis focusing on pre-release data & smart money movements

A comprehensive analysis of the major Forex currency pairs

Onidul Islam Siyam

July 20, 2025

Fundamental Priority:

The strongest fundamental drivers for the weeks are centered around interest rate expectations, inflation data, central bank policy updates, trade/tariff developments, and geopolitical risks. Below, I outline the key catalysts for each currency pair, including pre-release whispers and upcoming data/events ranked by expected impact.

EUR/USD Fundamental Drivers:

Interest Rate Expectations: The ECB is expected to maintain a dovish stance, with markets pricing in 110 bps of rate cuts for 2025, compared to only 44 bps for the Fed. This policy divergence supports USD strength.

Inflation Data: Eurozone CPI data (July 22, 2025) is forecasted at 2.4% YoY, slightly below consensus (2.5%). A softer-than-expected print could weaken the Euro further. Early whispers from Eurozone business surveys suggest cooling inflation pressures due to weak PMI data.

Central Bank Updates: ECB President Lagarde’s speech (July 24, 2025) may hint at further easing if growth weakens, potentially pressuring EUR/USD. Watch for any dovish surprises.

Trade/Tariff Developments: Reports of former President Trump advocating for higher tariffs on EU imports could dampen Eurozone export sentiment, weighing on EUR.

Geopolitical Risks: Receding geopolitical tensions (e.g., Middle East) shift focus to US trade policy, which may strengthen USD.

Pre-Release Data: Early indications from Eurozone PMI data (July 21, 2025) suggest manufacturing PMI may come in at 45.2, below consensus (45.8), signaling economic weakness. This could pressure EUR/USD before the official release.

Upcoming Events (Impact Ranking):

Eurozone PMI (July 21): High impact. Weak data could push EUR/USD below 1.1600.

ECB Lagarde Speech (July 24): Medium impact. Dovish tone could accelerate EUR selling.

US CPI (July 23): High impact. A hotter-than-expected print (forecast: 2.7% YoY) could boost USD further.

GBP/USD Fundamental Drivers:

Inflation Data: UK CPI rose to 3.6% YoY (July 15 data), above consensus (3.4%), supporting GBP temporarily. However, GBP/USD broke key technical support due to USD strength and widening US-UK yield spreads.

Central Bank Updates: Bank of England (BoE) meeting (July 31, 2025) is critical. Markets expect a hawkish hold at 4.75%, but any dovish shift could weaken GBP.

Trade/Tariff Developments: Brexit-related uncertainties and potential US tariffs continue to weigh on GBP sentiment.

Geopolitical Risks: Minimal direct impact, but global risk-off sentiment could pressure GBP as a risk-sensitive currency.

Pre-Release Data: UK jobs data (July 22, 2025) may show unemployment steady at 4.4%, but wage growth is rumored to be softer (5.2% vs. 5.5% forecast). A miss could weaken GBP before the release.

Upcoming Events (Impact Ranking):

UK Jobs Data (July 22): High impact. Softer wages could push GBP/USD toward 1.3300.

BoE Meeting (July 31): High impact. Hawkish hold supports GBP; dovish signals trigger selling.

US CPI (July 23): Medium impact. Strong US data could exacerbate GBP/USD downside.

USD/JPY Fundamental Drivers:

Interest Rate Expectations: The Bank of Japan (BoJ) is expected to forgo rate hikes in 2025 due to weak inflation and economic concerns over US tariffs. Fed’s hawkish stance (two cuts expected in 2025) supports USD/JPY upside.

Inflation Data: Japan’s CPI (July 25, 2025) is forecasted at 1.8% YoY, below the BoJ’s 2% target, reinforcing dovish policy expectations.

Geopolitical Risks: Japan’s political uncertainty (LDP lacking a parliamentary majority) could weaken JPY if fiscal expansion is signaled.

Trade/Tariff Developments: US tariff threats on Japanese exports (e.g., autos) are pressuring JPY.

Pre-Release Data: Early signals from Japan’s PMI (July 23, 2025) suggest a contraction (48.5 vs. 49.0 consensus), which could weaken JPY before release.

Upcoming Events (Impact Ranking):

Japan PMI (July 23): High impact. Weak data could push USD/JPY toward 150.00.

US CPI (July 23): High impact. Strong US inflation supports USD/JPY bulls.

BoJ Policy Update (July 30): Medium impact. Dovish stance could sustain JPY weakness.

AUD/USD Fundamental Drivers:

Commodity Prices: Australia’s economy is tied to metals/minerals. Falling iron ore prices (down 5% MoM) are pressuring AUD.

Trade/Tariff Developments: US-China trade agreements (finalized May 2025) reduce AUD downside risks, but ongoing tariff talks with other partners could add volatility.

Interest Rate Expectations: Reserve Bank of Australia (RBA) is expected to hold rates at 4.35%, but markets are pricing in a potential cut by Q4 2025, capping AUD upside.

Pre-Release Data: Australia’s employment data (July 24, 2025) may show a job gain of 20K (vs. 25K forecast). A miss could weaken AUD pre-release.

Upcoming Events (Impact Ranking):

Australia Employment (July 24): High impact. Weak data could push AUD/USD below 0.6600.

US CPI (July 23): Medium impact. Strong US data pressures AUD.

China PMI (July 31): Medium impact. Weak Chinese data could hit AUD due to trade ties.

USD/CAD Fundamental Drivers:

Commodity Prices: Canada’s oil-driven economy faces pressure from flat WTI prices (~$70/barrel).

Inflation Data: Canada’s CPI (July 22, 2025) is forecasted at 2.6% YoY, in line with consensus. A softer print could weaken CAD.

Central Bank Updates: Bank of Canada (BoC) is likely to hold rates at 4.25% (July 23, 2025), but dovish signals could emerge if inflation softens.

Pre-Release Data: Early whispers from Canada’s retail sales (July 21, 2025) suggest a 0.2% MoM decline (vs. 0.3% forecast), potentially weighing on CAD.

Upcoming Events (Impact Ranking):

Canada CPI (July 22): High impact. Soft inflation could push USD/CAD toward 1.3750.

BoC Meeting (July 23): High impact. Dovish tone accelerates CAD selling.

US CPI (July 23): Medium impact. Strong US data supports USD/CAD upside.

USD/CHF Fundamental Drivers:

Safe-Haven Flows: CHF’s safe-haven status is under pressure as geopolitical risks recede, supporting USD/CHF upside.

Interest Rate Expectations: Swiss National Bank (SNB) is expected to maintain ultra-low rates (0.25%), while Fed’s hawkish stance supports USD.

Inflation Data: Swiss CPI (July 24, 2025) is forecasted at 1.2% YoY, below consensus (1.4%), potentially weakening CHF.

Pre-Release Data: Early indications from Swiss business sentiment surveys (July 22, 2025) suggest a slight downturn, which could pressure CHF pre-release.

Upcoming Events (Impact Ranking):

Swiss CPI (July 24): High impact. Soft data could push USD/CHF above 0.9000.

US CPI (July 23): High impact. Strong US inflation supports USD/CHF bulls.

SNB Policy Update (July 31): Low impact. No rate changes expected.

NZD/USD Fundamental Drivers:

Commodity Prices: New Zealand’s dairy-driven economy faces pressure from softening global dairy prices (down 3% MoM).

Interest Rate Expectations: Reserve Bank of New Zealand (RBNZ) is expected to hold rates at 5.5%, but markets are pricing in a potential cut by Q1 2026, capping NZD upside.

Trade/Tariff Developments: NZD is sensitive to US-China trade dynamics due to export reliance on China.

Pre-Release Data: NZ trade balance (July 25, 2025) may show a wider deficit (-NZ$1.2B vs. -NZ$1B forecast), potentially weakening NZD.

Upcoming Events (Impact Ranking):

NZ Trade Balance (July 25): High impact. Wider deficit could push NZD/USD below 0.5900.

US CPI (July 23): Medium impact. Strong US data pressures NZD.

China PMI (July 31): Medium impact. Weak Chinese data hits NZD.

Actionable Insight: Short NZD/USD on a weak trade balance or fading rallies below 0.6000.

Sentiment Analysis:

Institutional Sentiment vs. Retail Positions:

EUR/USD: COT reports (July 15, 2025) show hedge funds increasing net-short Euro positions, aligning with retail traders’ bearish bias. This convergence suggests limited upside unless a major catalyst (e.g., strong Eurozone PMI) emerges.

GBP/USD: Hedge funds are net-short GBP, but retail traders are mixed, with 60% holding long positions. This divergence suggests potential for a squeeze if UK data surprises positively.

USD/JPY: Institutional players are heavily long USD/JPY, with COT data showing increased speculative positions. Retail traders are also bullish, indicating overcrowding and potential for a pullback if resistance holds.

AUD/USD: Hedge funds are reducing AUD longs due to commodity price weakness, while retail traders remain cautiously bullish (55% long). This divergence could signal a bearish move if data disappoints.

USD/CAD: Institutional sentiment is bullish on USD/CAD, with COT reports showing increased long positions. Retail traders are split, suggesting room for upside if fundamentals align.

USD/CHF: Hedge funds are net-long USD/CHF, aligning with retail bullishness (65% long). This consensus could amplify moves if Swiss data weakens.

NZD/USD: Institutional players are trimming NZD longs, while retail traders are 60% long, indicating potential downside if trade data disappoints.

Smart Money Movement:

EUR/USD: Smart money (e.g., hedge funds) is targeting liquidity below 1.1600, with large sell orders noted in options markets around 1.1550. Watch for a break below this level for institutional selling.

GBP/USD: Institutional selling is evident around 1.3450, with options positioning showing put buying at this level. Smart money may push for a break below 1.3400.

USD/JPY: Large buy orders are clustered around 148.50-149.00, suggesting smart money is betting on a breakout toward 150.00 if US data supports USD.

Global Risk Appetite (VIX, Equities):

The VIX is stable at ~15, indicating moderate risk appetite. Equities are mixed, with US indices flat and European indices under performing, supporting USD strength.

News tone is bearish on EUR and GBP due to trade and inflation concerns, while JPY faces pressure from dovish BoJ expectations. AUD, CAD, and NZD are weighed by commodity price softness.

Technical & Structural Edge:

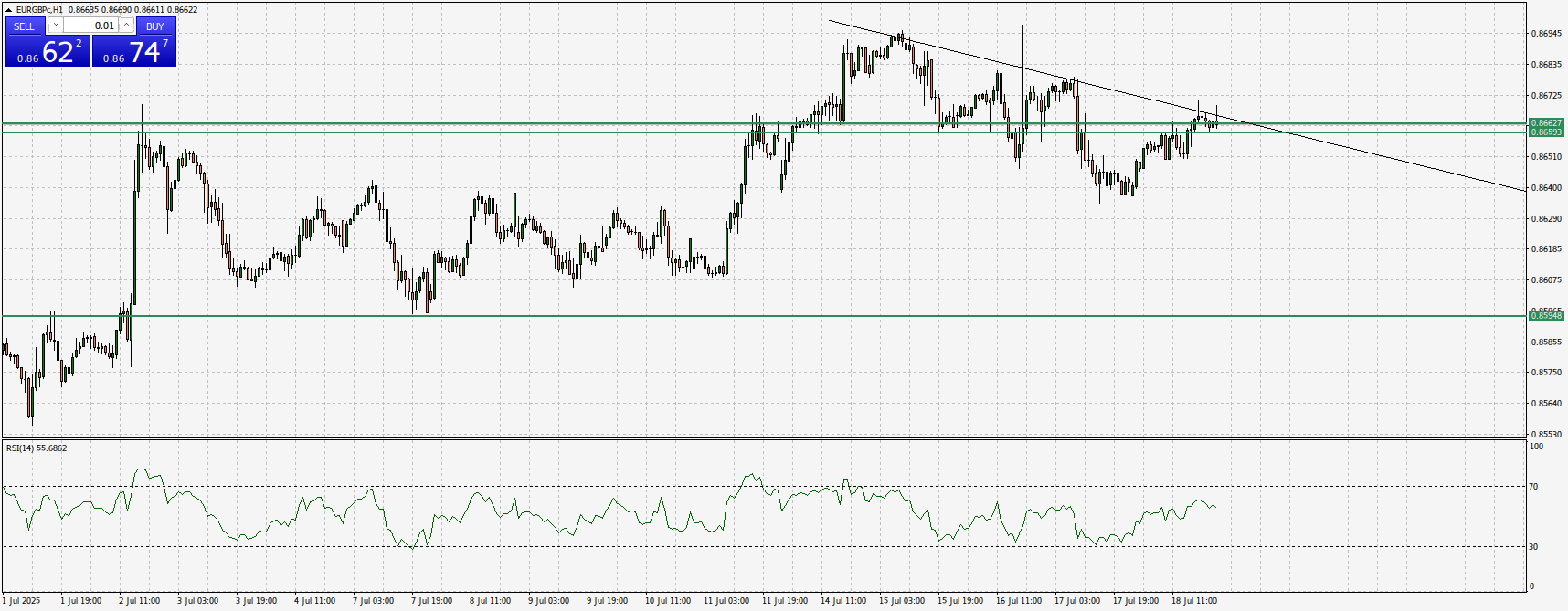

EURGBP:

EURGBP Might tend to bearish movement. Stay updated: UK Jobs Data (July 22): High impact. Softer wages could push GBP/USD toward 1.3300. And US CPI (July 23): Medium impact. Strong US data could exacerbate GBP/USD downside.

EURGBP 1 HOUR CHART

EUR/USD:

Chart Structure: Bearish, testing support at 1.1610 (200-period SMA). RSI above 50 but losing momentum.

Trend line, Breaking major swing low and pull back to test that level for two time (Double top). This level is also recognized by Fibonacci 38.2 level and it’s a proven strong price reaction zone. Indicate that price is now ready to go down.

EURUSD H4 CHART

A clear divergence is showing on 15 Minutes chart.

EURUSD 15 MINUTE CHART

GBP/USD:

Chart Structure: Bearish, trying to break below 1.3400 trendline support. Strong fundamental change and Market sentiment will help to break this level.

This analysis integrates real-time fundamental catalysts, pre-release data signals, institutional sentiment. And a little technical obsession. Ans not trading signal or investment advice. Stay vigilant for breaking news and adjust positions based on confirmed data releases. If you are a CFD trader Include proper risk management system in your strategy. Do your own research before executing any trade.

Hope this Analysis and Provided Information will help you to become ready to trade this week.

Thanks,

@anidsiam from @finovatic